Platinum Group Metals: automotive market continues to shape demand

The precious metals complex in 2018 has come under pressure from the stronger US Dollar amidst the rising rate environment. Platinum and palladium have led the declines with a performance of -16% and -18.3% Year-to-Date (YtD). In addition to the strong US Dollar, platinum’s performance in particular has been dampened by extreme negative sentiment, weak fundamentals, and gold’s lacklustre performance. In lockstep with platinum, its sister metal palladium being a more industrialised precious metal has suffered from repercussions of the tit for tat trade wars. We believe not much has changed from a fundamental perspective for palladium and its outlook looks much brighter in comparison to platinum. The platinum market is expected to see another year of surplus, marking its fourth year in a row. Meanwhile the palladium market is expected to remain in a deficit this year for the 7th consecutive year in a row. We expect, palladium prices might have a higher chance of recovery when the negative sentiment from the trade spat dissipates, as demand remains on a solid footing.

Given the extensive use of platinum (nearly 40%) and palladium (nearly 70%) in vehicle catalytic convertors, their demand appears to be particularly sensitive to the trend in global auto sales. Gasoline powered catalytic convertors utilise either platinum or palladium in combination with rhodium, whereas diesel powered catalytic convertors and diesel particulate matter filters predominately use platinum and require a greater quantity of the Platinum Group Metals (PGMs) in comparison to gasoline powered cars. While auto sales in both US and China have been strong in 2018, both these markets are dominated by gasoline powered vehicles that utilise palladium in the catalytic convertors to reduce harmful emissions. At the same time, the platinum intensive diesel car market has witnessed its market share decline 17% Year-on-Year (YoY) in the first quarter of 2018. A large portion of this decline in market share can be attributed to the dieselgate scandal1 sparked by Volkswagen in 2016. In addition, the gradual adoption of electric vehicles is also expected to further reduce market share of diesel vehicles. Commitments from Norway, Britain, France and India to the end of the sale of gas and diesel vehicles over the next 10 years and transition into the electric vehicle market are weighing on the demand story for platinum.

Figure 1: New passenger cars by fuel type in the EU, market share (%)

Source: Bloomberg, WisdomTree, data available as of close 06 August 2018.

Historical performance is not an indication of future performance and any investments may go down in value.

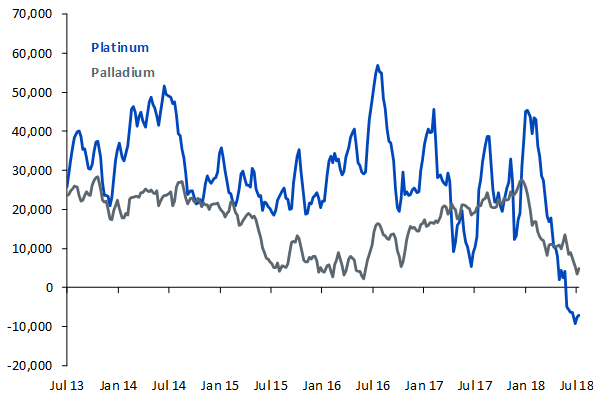

According to the Commodity Futures Trading Commission (CFTC), net speculative positioning on platinum futures have declined to -7146 contracts, more than 2x standard deviations below the five-year average (as of 31 July 2018). While platinum has historically traded at a significant premium over gold, its currently trading at a steep discount to gold which is now hovering close to its record high at US$384 (as of 6 August 2018). Gold’s weak price performance owing to the rising rate environment has remained a strong headwind to platinum’s price appreciation. At current levels, we expect short covering could support some upside in the near term. However, we expect the structural change in the auto market, the stronger US Dollar and the ongoing supply surplus to cap further upside in platinum prices over the long run. A similar trend has been observed for palladium futures as net speculative positioning has dropped 1x standard deviation below the five-year average to 4913 contracts (as of 31 July 2018) underpinning the extent of negative sentiment within the PGMs.

Figure 2: Net positioning for platinum and palladium underpins extent of negative sentiment

Source: Commodity Futures Trading Commission (CFTC), Bloomberg, WisdomTree, data available as of close 06 August 2018.

Historical performance is not an indication of future performance and any investments may go down in value.

We believe platinum and palladium could be at the cusp of a recovery as sentiment is unjustifiably low. As the interest rate trajectory in the US has been priced in for the rest of the year, we expect that the easing US Dollar might provide further tailwind for the precious metals. However, among the two metals palladium could stage a long and more sustained recovery as its underlying fundamentals remain supportive.

1 Refers to legal action from the US Justice Department against Volkswagen and its subsidiaries for violating climate protection regulation.

Related Blogs