What's Hot: The stakes are high for the widow maker trade

The widow maker trade is back. At over 136 yen to the US dollar, the yen is approaching levels of weakness last seen in the summer of 1998. Investors are now betting that the Bank of Japan (BOJ) under growing pressure to stabilise the yen will have to abandon its 0.25% cap on benchmark bond yields and allow them to rise. If this were to happen, it would have widespread ramifications allowing the yen and Japanese rates to rise.

BOJ’s unprecedented quantitative easing program is getting harder to defend

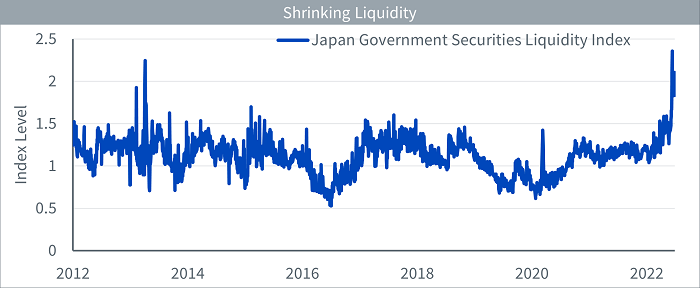

The BOJ kept its bond purchase plan unchanged for the July-September quarter, even though its actions are weighing on the yen. It insists the Japanese economy still needs support. While this is true, the BOJ needs to take a balanced approach by considering both the merits and side effects of its ultra-easy monetary policy. As it stands, liquidity deteriorated on the JGB market and the weaker yen continues to drive up imported inflation. The BOJ spent more than ¥16Trn (US$118Bn), its largest monthly purchase in June since Governor Haruhiko Kuroda took the helm of the BOJ in 2013, as it sought to suppress yields. The JGB market faces continued pressure with a gauge of liquidity pointing to worst levels since 2013. A rise in the index implies a decline in liquidity.

Source: Bloomberg, WisdomTree as of 1 July 2022.

Historical performance is not an indication of future performance, and any investments may go down in value.

Inflation becoming a concern

A gauge of Japan’s inflation expectations has climbed to a seven-year high, as a weak yen compounds the effect of elevated commodity prices. In Tokyo, the core CPI (excluding only fresh food) increased 2.1% YoY in June, picking up from a 1.9% YoY rise in May. The boost from energy prices barely changed owing to government subsidies for oil wholesale companies. The June BOJ tankan (short term economic outlook), showed business confidence Diffusion Index (DI) among large manufacturers decline in June for a second quarter in a row owing to parts shortages, surging raw material costs and lockdowns in China. With raw material prices surging and the yen depreciating, the output price DI continued to show pass-through of higher costs to sales prices, and corporate inflation expectations increased further.

BOJs containment of yields becoming a costly affair

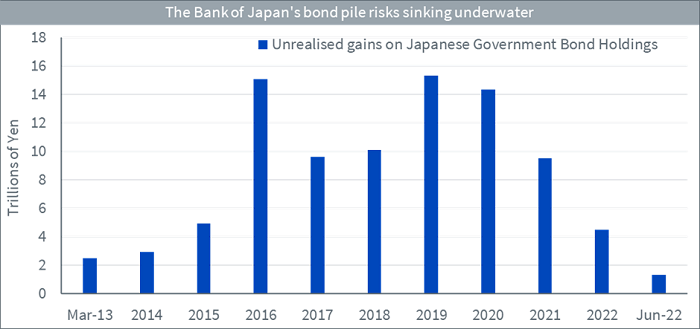

By implicitly capping 10-year Japanese government bond yields at 0.25%, the Bank of Japan (BOJ) is struggling against the tide of rising global interest rates. In doing so, the BOJ now owns almost half of all Japanese government bonds (JGB).

Source: Bank of Japan, Mizuho Securities, WisdomTree as of 30 June 2022. Please note: the estimated June 2022 figure does not reflect price changes on bonds bought after March.

Historical performance is not an indication of future performance, and any investments may go down in value.

This could spell trouble for the Japanese government as it relies on the BOJ indirectly underwriting its spending with large debt purchases. According to Mitsubishi UFJ, the BOJ may have been saddled with as much as ¥600Bn (US$4.4Bn) in unrealised losses on its JGB holdings earlier this month, owing to the widening gap between domestic and overseas monetary policy. They estimate if 10-year yields reach 0.65%, paper losses on JGBs could exceed the BOJs capital base, which totalled ¥10.9trn at the end of March. As the BOJ’s own calculations use book value as opposed to market value, it reflects no change in its finances.

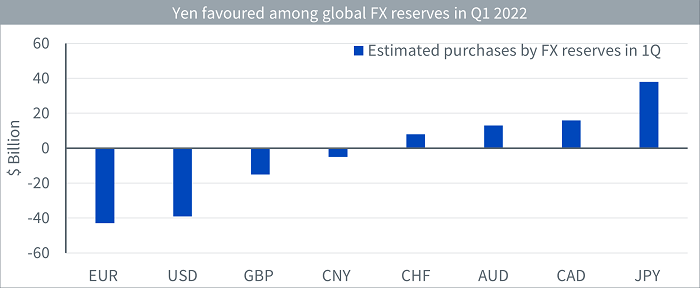

Yen remains a favourite habitat of FX reserves in Q1

According to the IMF, global FX reserves managers sold euros, US dollars, and pounds in Q1 2022 and bought more yen than any other currency making it a favourite habitat of FX reserves. FX reserves probably had to shore up a decreased share of yen assets owing to the yen’s decline. Persistent demand from reserve managers alongside Japan’s status as the world’s largest net creditor may also help provide a floor for further downside.

Source: Bloomberg, International Monetary Fund (IMF).

Please note: Purchases are estimated by adjusting IMF data for currency fluctuations and return on short-term government bonds.