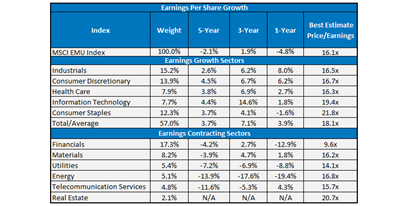

Where Is Earnings Growth in the Eurozone?

There are several reasons to be optimistic about the prospects for Eurozone equity markets: market multiples are low, bond yields are low (and even negative out to 10-year maturities in Germany) and earnings trends are looking more positive. That last item is especially important. Simply looking at the earnings for broad market indices like the MSCI EMU Index may give a distorted view of what is happening across a number of sectors in Europe. Looking at the earnings figures for the MSCI EMU Index, one can see earnings declining over the last five years at a rate of -2.1% per year. But half the sectors in the market (typically the export-oriented sectors) are delivering earnings growth that ranges from 2.6% per year to 4.5% per year and on average is 3.7% per year. These export-oriented sectors are Consumer Discretionary, Industrials, Health Care, Information Technology, and Consumer Staples. These sectors constitute roughly 57% of the weight of the MSCI EMU Index. On the other hand, there are sectors (the other 43% of the MSCI EMU Index) in which earnings have collapsed: Financials, Energy, Materials, Utilities, and Telecommunications. The Financials sector was the biggest of these from a weighting perspective.

Source: Bloomberg as of 28/09/16. Past performance is not indicative of future results. You cannot invest directly in an index.

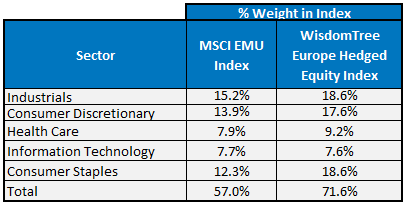

Focusing on Eurozone Earnings Growth

The WisdomTree Europe Hedged Equity Index (“Eurozone Exporters”), which is composed of multinationals within the Eurozone, is achieving earnings growth largely because it is under-weight these predominantly domestic sectors. These sectors are exposed to a more challenged earnings environment whilst the index is tilted towards sectors where. earnings have been growing in the Eurozone. Compared to the 57% of the MSCI EMU Index allocated to those sectors with positive earnings growth, the WisdomTree Europe Hedged Equity Index currently has 72% allocated to these sectors. Notably, the index is underweight in Energy and Financials and this has helped introduce a quality bias to the portfolio. For those who believe valuations are low in the Eurozone, the large capitalisation multinationals with an export tilt represent one segment of the market with a better earnings growth environment. This strategy is currently represented by the WisdomTree Europe Hedged Equity Index.

Tilting Toward Positive Earnings Growth Sectors

Source: Bloomberg as of 28/09/16. Subject to change

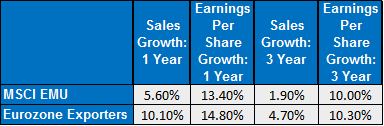

The sector tilt of the Eurozone exporters, with its focus on positive earnings growth and above average sales growth is apparent on both a one year and three-year time horizon. Compared to MSCI EMU, the WisdomTree strategy is usefully positioned to focus on a higher quality sector mix and stronger fundamentals.

Source: Bloomberg as of 28/9/16. Past performance is not indicative results. You cannot invest directly in an index.

For those investors sharing this sentiment:

- WisdomTree Europe Equity UCITS ETF – EUR Acc (HEDF/HEDG)

- WisdomTree Europe Equity UCITS ETF – USD Hedged (HEDJ)

- WisdomTree Europe Equity UCITS ETF – GBP Hedged (HEDP)

- WisdomTree Europe Equity UCITS ETF – CHF Hedged Acc (HEDD)