How to position around Europe’s recovery: buy small-caps and overweight the discounted cyclicals

Europe may have reached an inflection point

The Eurozone economy has become increasingly reliant on the strength of overseas markets to counter the prolonged shortfall in domestic spending at home. Underscoring the region’s economic weakness is the Eurozone’s third consecutive month of deflation. Moreover, Greece’s place in the Eurozone remains uncertain, in spite of the four month bailout extension granted by Eurozone members.

And yet, now rather than later, may be the best time to buy into Europe’s domestic recovery.

This month’s first QE injection of 60 billion euro coincides with a markedly depreciated euro and indications that Brussels is allowing more leeway towards fiscal consolidation. As countries like France and Italy are given more time to reduce their budget deficits, the EU is actively promoting more investment spending through state-sponsored guarantees and investment vehicles. Alongside this, signals are emerging that the European economy has started to strengthen. In particular, the supply of credit, a key gauge for domestic economic activity has expanded in recent months.

Over the last three months (from November 2014 to January 2015), loans issued by banks have risen by EUR 313 billion, which is a marked reversal from the EUR 1.7 trillion of loans being withdrawn from the economy since 2012 (see chart 1). This presents an opportunity for Europe’s ‘bank-finance reliant’ small businesses to get a funding boost, and complement a prolonged period of export-led growth with domestic demand-led growth.

European shares lost momentum in H1 2014 as a higher euro undermined their ability to absorb the slack at home with overseas exports. But the marked devaluation of the euro since has revived sentiment in European shares. At this inflection point, European small-cap stocks, more so the large-caps that are known to be less exposed to the local economies, are likely to benefit the most. Already, European small-cap stocks have started to recapture the interest of investors, having rebounded more strongly than European large-cap this year on the back of improved credit conditions in Europe. As shown in chart 1, the index of WisdomTree Europe SmallCap UCITS ETF is up 6.7% YTD and 14.8% from its last years’ trough (on 16 October 2014).

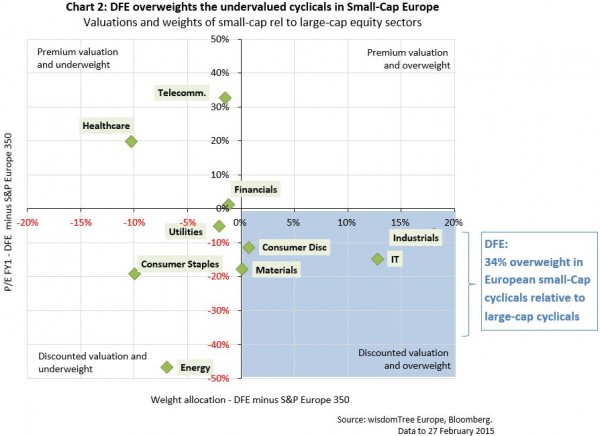

Capitalising on a broad-based recovery: overweight cyclical sector at discounted valuations

Successful positioning around Europe’s rebounding economy should include an allocation with a cyclical bias against reasonable valuations. Investors seeking a cost-effective means to attain such an exposure should buy into ETFs. However, buying ETFs tracking conventional market-cap weighted benchmarks may not offer enough of a cyclical rebound tilt for investors, or a rebalancing strategy that emphasises allocations into value-orientated quality stocks. When weighted by market cap, there is a risk that, amidst the upturn cycle, investors’ small-cap stock portfolio becomes overrepresented by richly valued companies. Expensive stocks are not ideal for those investors who desire more evidence of sustainable recovery in Europe, before they invest: especially as, market-cap weighted benchmarks rewards companies with a higher weight when the share prices rise, irrespective of whether fundamentals have kept pace with share appreciation or not.

However, there are alternatives for investors seeking a more quality-orientated solution to ride the upturn. Such a strategy emphasizes a weighting approach not by market capitalisation, but by a transparent, well-understood company fundamental: cash dividends. The WisdomTree Europe Small-Cap UCITS ETF (DFE) employs such a strategy. Below we discuss DFE’s index and contrast it to a large-cap, market-cap weighted benchmark that a conventional ETF would track.

The chart below (Chart 2), shows that on the x-axis, DFE is overweight in the cyclical sectors relative to a market cap weighted European large-cap equity index such as the S&P Europe 350. For instance, DFE is relative overweight consumer discretionary, IT, materials and industrials by a combined 34%. Together the cyclical sectors make up 65% of the cash-dividend weighted index of DFE . Evidently, the strong cyclical bias means DFE is also underweight in defensive sectors of telecom and healthcare. While exposure to financials is not far off from that of its large-cap equity benchmark equivalent, this is mainly because a tough regulatory environment, equity recapitalisation and balance sheet deleveraging has caused many to cut, if not suspend dividends. Hence, too few financial stocks have made it into the basket with sizable weights. It is likely that, underpinning the recovery in loan growth, banks’ rising profitability will also restore the dividend policy and in the process see DFE increase its allocation in financials.

Interestingly, the cyclical sectors of Europe’s small-cap stock universe, trade at relative low forward earnings valuations. As shown on the Y-axis of chart 2, IT, Consumer discretionary and Materials have valuations that are anywhere between 10 to 20% discounted to the valuations of large-cap sector equivalents. Industrials, DFE’s largest overweight within the small-cap sectors, are trading at an 8% discount to large-cap industrials. At a time when Europe’s economy is showing no evidence of broad based recovery and is entirely dependent on exports, the market appears to be rewarding Europe’s large-caps cyclicals on the premise that their global footprint and export exposure outside the European region, most notably to the US and China, is a better investment proposition. However, if the economy of Europe has indeed reached its inflection point, it will be the cyclicals within the Europe’s small-cap equity universe that stand to benefit investor’s the most longer-term; especially when a dividend screen helps to exclude the speculative nature of many of those companies, leaving the investor with a quality basket to capitalise on Europe’s longer term recovery potential.

Investors sharing this sentiment may consider the following UCITS ETF:

All data is sourced from WisdomTree Europe and Bloomberg, unless otherwise stated.