Two years of PCOM: outperforming peers through innovation

Why broad commodities?

Insights from our recent survey1 revealed that 29% of investors don't allocate to commodities. Broad commodities have historically displayed equity-like returns, constituting an effective inflation and geopolitical hedge with low correlation to other asset classes. For these reasons, we think that a diversified exposure to commodities can significantly improve the risk-return profile of a portfolio. On top of that, commodities have historically been one of the best performing asset classes during the late stages of the economic cycle.

PCOM’s 2nd anniversary

Two years ago, we launched a product with the aim of innovating in the delta 1 broad commodity space: the WisdomTree Broad Commodities UCITS ETF (PCOM). Offering an innovative solution, this ETF is designed for investors seeking to improve their commodities performance while minimising tracking error against the Bloomberg Commodity Total Return Index (BCOMTR Index). PCOM's proposition is simple. It replaces the synthetic gold and silver exposure of the Bloomberg Commodity Index ("BCOM") with a physical one.

Physical or synthetic?

The fundamental concept underpinning the fund is inspired by a key question in commodity investing: how should an investor pursue exposure to commodities? There are typically three options: direct physical investments, commodity futures and commodity-linked equities.

Commodity-linked equities often fail to offer a true exposure to commodities, with their correlation primarily aligning with broad equity markets rather than commodities indices, plus they mostly reflect company management and practices, often involving hedging strategies that compromise direct commodity exposure.

While the idea of buying commodities directly may seem intuitive, it is, in practice, highly challenging, if not impossible. Obtaining direct exposure to natural gas would require receiving, maintaining, and storing the gas until selling. Generally such a process is not a viable option for most investors. In addition, investing in broad commodities encompasses numerous commodities, each requiring specialised storage facilities, rendering physical investment both costly and logistically challenging.

In contrast, investing in futures contracts is significantly more operationally feasible. Futures contracts generally offer greater liquidity than physical commodities and involve fewer regulatory obstacles. Moreover, investing in commodities through futures has historically provided performance benefits (see Figure 1).

Figure 1 – Historical risk premium in broad commodities

Source: Bloomberg, WisdomTree. Start date: 04/01/1960; end date: 31/10/2023. Historical performance is not an indication of future results and any investments may go down in value.

The reasons behind this overperformance have been widely discussed in the academic literature. Keynes (1930) and Hicks’ (1939)2 theory of normal backwardation postulated that a risk premium would, on average, accrue to the buyers of futures. The theory explains that in order to insure themselves from a decline in the commodity price, commodity producers may want to enter into a future short position, which is an agreement to sell a commodity at a specific date in the future at an agreed price. On the other side, commodity consumers may want to enter into an opposite (long) position to insure against increases in the spot price. Keynes claims that the hedging pressure applied by producers overpowers the one applied by consumers. The resulting net short hedging position will lower the price of the futures compared to the expected future spot price. By “backwardating” the futures price relative to the expected future spot price (that is where the term “normal backwardation” has come from and refers to the expected spot price, not current spot price), futures investors would receive a risk premium from producers for assuming the risk of price fluctuations.

In the literature, many researchers have attempted to estimate this risk premium, and it is well established that it varies in size, time, and across different commodities3. But the clearest exception to the normal backwardation theory is precious metals. Empirical research4 covering the period 1980-2005 found no evidence of a risk premium in gold futures over spot prices. This discrepancy is attributed to the limited hedging activity by gold miners, diminishing the value of gold futures to producers.

Do the numbers corroborate this theory?

Figure 2 - The physical premium

Source: Bloomberg, WisdomTree. Start date: 04/06/2007; end date: 31/10/2023. Historical performance is not an indication of future results and any investments may go down in value.

Over the past 15 years, gold and silver spot have outperformed their synthetic counterparts and did so in a consistent way. Figure 2 shows the historical outperformance of the spot price of gold and silver compared to a fully funded synthetic exposure for investment. Since 2007, physical gold and silver consistently outperformed the synthetic gold and silver, and they did so across very different market regimes.

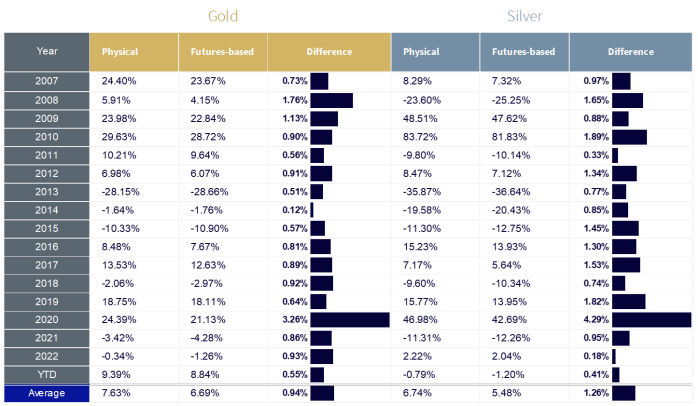

Table 1 – Spot vs. Future year by year

Source: Bloomberg, WisdomTree. Start date: 04/06/2007; end date: 31/10/2023. Historical performance is not an indication of future results and any investments may go down in value.

Looking at Table 1, we can see how a physical investment in gold or silver has overperformed the synthetic exposure in all of the past 15 years. On average, physical gold performed better than futures-based gold by 0.96%, while physical silver overperformed by 1.28%.

Hypothetically speaking, what would the additional performance have been if you'd replaced the synthetic exposure to precious metals with a physical one in BCOM (until the launch of PCOM)?

In the chart below (Figure 3) we show exactly this. This enhancement would have added 17 basis points (bps) on average since 2007. If we exclude the impressive performance of 2020, the spot contribution hovered around 10 bps since 2007 consistently.

Figure 3 – Spot vs. future yearly contribution

Source: Bloomberg, WisdomTree. Start date: 04/06/2007; end date: 31/10/2023. Historical performance is not an indication of future results and any investments may go down in value.

But what about the performance since the launch of the ETF? As we can see in the next figure, the enhancement added 39 bps to the product performance, which is in line (and even slightly better) with what our analysis suggested.

Figure 4 – Spot vs. future yearly contribution

Source: Bloomberg, WisdomTree. Start date: 06/12/2021; end date: 31/10/2023. Historical performance is not an indication of future results and any investments may go down in value.

Operational set-up

Operationally, the fund combines a synthetic exposure to the ex-precious metals component of the Bloomberg Commodity Index5 and a physical exposure to gold and silver through investments in physically backed ETPs6. The management fees amount to 19 bps, while the swap fees are 12 bps, but they are only paid on the ex-precious metals portion of the ETF, effectively bringing this figure down to less than 10 bps.

Conclusion

We launched PCOM to offer a way for investors to enhance their broad commodities exposure. The idea of the fund is simply to hold physical gold and silver, which has historically yielded a premium vs. holding futures. Since then, physical gold and silver kept outperforming their synthetical counterpart by the same magnitude as they did on average in the past 15 years.

Sources

1 WisdomTree, Censuswide. Pan-Europe Professional Investor Survey Research, Survey of 803 professional investors across Europe, conducted during August 2023.

2 Keynes, John M. (1930), A Treatise on Money, Vol. 2 (Macmillan; London) and Hicks, John R. (1939), Value and Capital (Oxford University Press; Cambridge).

4 Xu, H., Lin, E. C. & Kensinger, J. W., 2013. On the estimation of risk premium in the gold futures market: using the Goldman Sachs Commodity Index (GSCI) approach. Research in finance. Vol. 29., pp. 103-118.

5 On the relative collateral the fund and earns interest on a portfolio of 12 T-bills with various maturities, rolled bi-weekly, and with an average duration of 84 days.

6 When it comes to the implementation of an investment in physical commodities and physical precious metals, in particular,

investors can: 1. Own/rent a vault to store gold/silver bars: this solution is only available to extremely large investors, the cost of storage and the cost of insurance can be high and organising safe movement and delivery of large chunks of gold or silver is extremely difficult. 2. Invest in a physically-backed exchange-traded product (ETP): securities are backed by physical bars of the relevant metal and usually held by the custodian within a secure vault and regularly inspected by an independent entity. Exchange-traded commodities (“ETCs”) are operationally very easy to use. They are listed on exchange and trade like shares during market hours.

Related blogs