WisdomTree launches a US multifactor strategy

As we speak to clients approaching the second half of 2018, we tend to hear versions of a familiar refrain that we’ve heard for a few years:

US equities are in a late cycle rally. On the one hand, valuations are relatively high, but on the other, corporate fundamentals remain strong enough to justify stocks continuing to rally further.

The core of this statement causes massive indecision amongst investors who all tend to have some exposure to US equities. Is now the time to add even more? To trim? For new dollars coming into investment portfolios, what is the “right” decision to make regarding US equity exposure?

This could be one of the trickiest questions to answer today.

Momentum has been a GREAT trade!

One of the most positive consequences of the proliferation of different smart beta strategies is that today any investor can access tools that provide exposure to the longstanding, academically established factor premia:

- Quality

- Size

- Value

- Momentum

- Low Volatility

There are options that allow investors to even select baskets of stocks that represent individual factors. As a result, many have noticed that momentum has been a great trade during 2017 and into 2018 thus far.

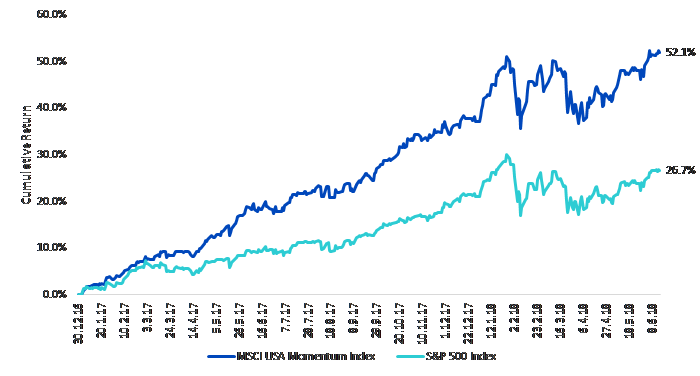

Figure 1: Momentum stocks have almost doubled the return of the S&P 500 over nearly 1.5 years

Source: Bloomberg, 31 December 2016 to 15 June 2018. You cannot invest directly within an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

In a way, the performance run of momentum stocks exemplifies the inherent challenge of the factors and having the individual options as tools within a portfolio toolkit. Momentum has historically outperformed—and it may continue to outperform for some time. Chasing it now after its rally doesn’t quite feel good as an investor, but not chasing it and watching its rally continue also does not feel good.

A new way to consider what “diversification” means

If we take a step back for a moment, with all that has been written about the different “factor premia”, it is important to remember that we still don’t know which might or might not outperform on a going forward basis. What we do know, at least, is what history has shown us thus far:

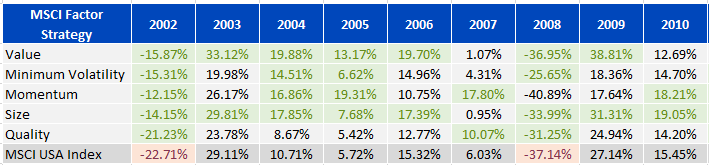

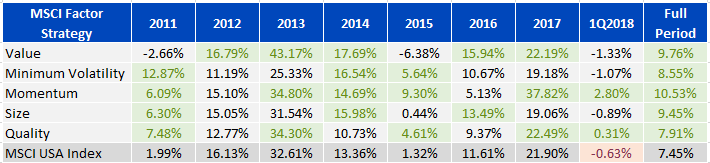

Over long periods of time, all five of the factors that we cited earlier in this piece have outperformed the market capitalization-weighted benchmark. We see that in figure 2:

Figure 2: It has been natural for factors to ebb & flow in their out (& under) performance

Source: MSCI. 31 December 2001 to 31 March 2018. The MSCI Factor strategies do represent underlying indexes and do include backtested returns. Value: MSCI USA Enhanced Value Index, which began live calculation on 12 Dec. 2014. Minimum Volatility: MSCI USA Minimum Volatility Index, which began live calculation on 2 June 2008. Momentum: MSCI USA Momentum Index, which began live calculation on 15 Feb. 2013. Size: MSCI USA Risk-Weighted Index, which began live calculation on 28 June 2011. Quality: MSCI USA Sector Neutral Quality Index, which began live calculation on 12 December 2014. Returns are calculated gross of tax withholdings due to data availability. You cannot invest directly within an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

Over time, the term diversification has evolved. Instead of holding a single company, investors thought to hold baskets of multiple companies to mitigate the risk of any single one. Instead of holding a single country or single sector, investors thought to hold baskets of stocks from multiple sectors and countries—again, to mitigate unique risks from a single sector or single market.

Because we know that factors ebb and flow in their outperformance and have tended towards long term outperformance, strategies that rebalance back to exposure across all factors could make a lot of sense if the goal is to limit the risk of sustained cycles of relative underperformance.

Enter WisdomTree’s US Multifactor Index

Now that the stage has been set, we will briefly detail WisdomTree’s unique solution to this problem with our first multifactor index to be launched in the European market.

Question: Which factors does WisdomTree’s index focus upon for selection purposes?

WisdomTree’s methodology explicitly focuses on four factors.

- Quality

- Value

- Momentum

- Correlation

Quality and value are factors that are focused on the fundamentals of firms, whereas momentum and Correlation are focused on technical aspects and past price behavior. Correlation is the only factor here not as much in the “mainstream” of factor discussions. In our view, firms with lower correlation to the market exhibit greater diversification characteristics and could have some risk mitigation properties from a portfolio perspective.

Bottom Line: every constituent within the WisdomTree US Multifactor Index was ranked across all four of these factors, and the approach does not assemble groups of stocks that may look strong on a single factor, only to be mixed with firms strong on the others.

Question: How does WisdomTree’s index combine and refresh the factors?

On a quarterly basis, the 800 largest eligible stocks by market capitalization are screened, with the top 200 qualifying for the WisdomTree US Multifactor Index based on their scores across all four factors. Additionally:

- Each of the 200 stocks is given a volatility score, based over the past 12-month period. Lower volatility leads to a higher score, helping WisdomTree tap into the “low volatility” factor without explicitly stating it as a factor.

- Index weighting is based on the combination, equally split, of the composite score of the firm across the four factors and the volatility score. Relatively strong factor scores PLUS low volatility is the road to greater weight. Note that neither of these aspects is sensitive to the size of the firm, so WisdomTree taps into the “size” factor without explicitly stating it as a factor.

- Finally, the weights of constituents are adjusted such that the final index is sector-neutral relative to a market capitalization-weighted universe.

WisdomTree is excited about broadening the scope of its equity index repertoire with its first multifactor index launched in European markets. We believe that it represents the next step in innovation that relates to building equity indexes.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.