Gold outlook for Q4 2020: Trade turbulence and Middle East tensions still to dominate

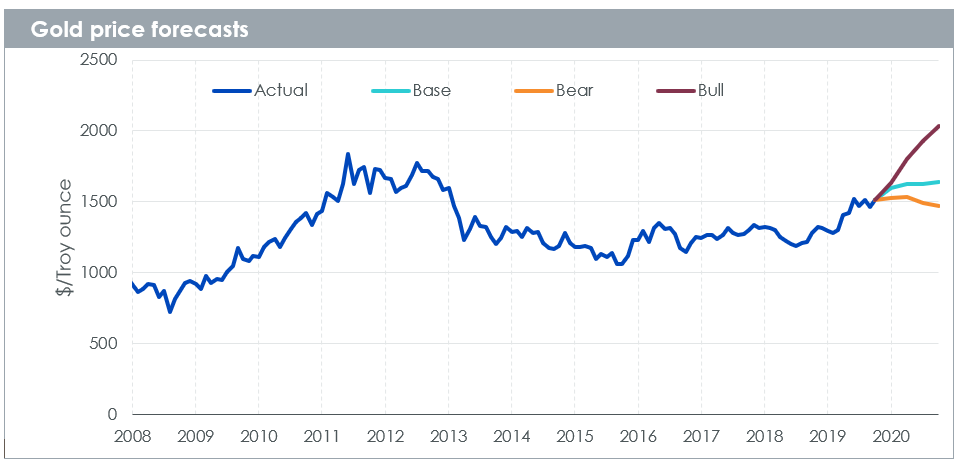

We ended 2019 with one crisis averted: US-China tariffs that were supposed to be ramped up on December 15th were cancelled as the two nations reached a “phase one” trade deal. But as 2019 came to a close and 2020 started, a crisis which had been brewing for some time in the background came to the foreground: tensions between US and Iran flared to levels not seen since 1979. Gold remained resilient when the trade fears subsided but accelerated when Iranian crisis started. Gold has risen to US$1593/oz on 7th Jan 2020, up from US$1461 on 9th Jan 2019.

We believe that the tensions in the Middle East and trade frictions will continue to support gold prices during 2020. The risks we highlighted in “40 Years of fraught US-Iran tension in the Persian Gulf plays on” are being played out. As the US-China phase one deal based on a narrow set of issues does not really address the full scope of grievances that the US has with China, it’s not surprising that the gold markets remains cautious about further trade progress being made. Indeed, a deal that is good enough for now could stall progress on further phases until after the Presidential election in the US (November 2020). Worse still, a vindicated Trump Administration, declaring a premature victory over China (after declaring trade victories with Mexico, Canada and a number of Asian countries), could sharpen its focus on its trade deficit with Europe in 2020, adding to the risks of economic deceleration in 2020. In “Market Outlook 2020: Trade truce or trade Armageddon?” we said that the direction of gold and other assets will heavily depend on the direction trade talks. That still remains the case: although we know some tariffs have been averted, in the absence of a comprehensive trade deal having been signed, trade protectionism could either increases or ease as negotiations continue.

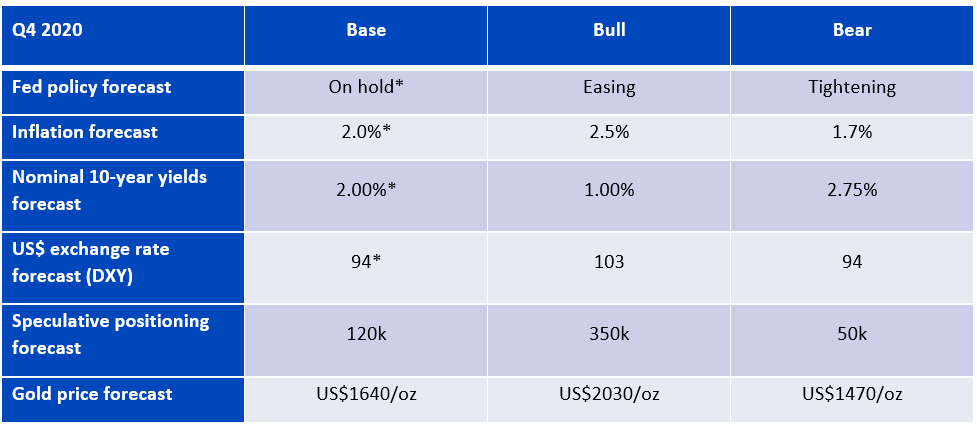

Our internal model indicates that gold prices are poised to move higher in 2020. Gold prices could end the year around US$1640/oz. We form that base case view using consensus forecasts for Treasury yields, the Dollar Basket, inflation and conservative forecasts for speculative positioning in gold futures. However, if we end up in a world where tensions in the Middle East persist or trade protectionism spirals out of control and monetary authorities have to resort to utilising radically new tools, we could see gold rising to over US$2000/oz. Conversely in a world where trade frictions are resolved amicably, gold could end 2020 around US$1470/oz.

In “Gold: how we value the precious metal”, we explain how we characterise gold’s past behaviour and if gold behaves in a consistent manner in the future, we can forecast the future trajectory of the metal if we have a view on its key drivers. Here are our forecasts in different scenarios:

Source: Bloomberg, WisdomTree. Actual data as of 31th December 2019

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties

Assumptions:

Source: Bloomberg, WisdomTree

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties

*Based on consensus forecasts taken from Bloomberg in December 2019

Summary of forecasts: at the crossroads

As we articulated in “Market Outlook 2020: Trade truce or trade Armageddon?”, the world economy is at a crossroad. Since we wrote that piece, we know we have reached a “phase one” trade deal between US and China, which removed the immediate risk of tariffs escalating in the very short-term. That risk has however been replaced by a risk of military confrontation between the US and Iran, which has driven the rally in gold in the past month. If global trade frictions continue to be resolved in an amicable manner, we could continue to see a recovery in a range of cyclical assets. A broad risk-on market would typically not favour gold. That is our bear case. Conversely if trade issues escalate again, possibly reflecting a failure to move beyond the first phase, all the fears of the economy stalling may return. We could see a strong policy reaction to fears of a manufacturing recession bleeding into the wider global economy. With current monetary policy space limited, the utilisation of new monetary tools and wider fiscal policy is likely to take place. That is likely to spook investors, driving up the demand for haven assets like gold. If tensions in the Middle East linger, that could compound investor anxiety. That is our bull case. But we don’t know which way things will turn. In a year of a US presidential election we believe that the US will likely aim to keep trade discussions ongoing with China to avoid tipping its economy into a recession, but that is not guaranteed. Also, Trump’s prior promises to keep the US out of unnecessary military conflicts, could lead to a de-escalation of tension as the election approaches. At this stage we don’t know what other phases of the trade deal will involve and therefore can’t rule out the deal unravelling. Comments by the US President before the phase one deal was reached, indicate that he is willing to wait until after the presidential election for a full deal to complete. As a base case we take consensus forecasts for all of the macro inputs to our model and then we pare speculative positioning down to 120,000 contracts (considerably lower than today’s elevated levels, but slightly above historic average). That reflects current concerns over Iranian tension and global trade subsiding.

Bear Case

In the bear case, the Federal Reserve (Fed) raises rates as an economic crisis is averted, reversing the cuts in 2019. Treasury yields rise as we look like we are on path of rate normalisation. Inflations slips as monetary policy is tightened and the tariffs are pared back (the tariffs would have otherwise increased the costs of goods in the consumption basket). Speculative positioning in gold falls considerably as experimental monetary policy is avoided and the US Dollar softens as demand for haven assets falls away.

Bull case

In the bull case, the Fed loosens policy is response to recession fears, pushing Treasury yields lower. Inflation rises as the tariffs applied to imported goods raise the cost of consumption basket. Moreover, the market fears inflation in the future could rise substantially in reaction to unconventional monetary policy. The US Dollar appreciates along with other haven assets like gold. Speculative positioning in gold remains as elevated as was in September 2019, reflecting the widespread anxiety and fears about the new monetary and economic paradigm on top of ongoing tension in Iran.

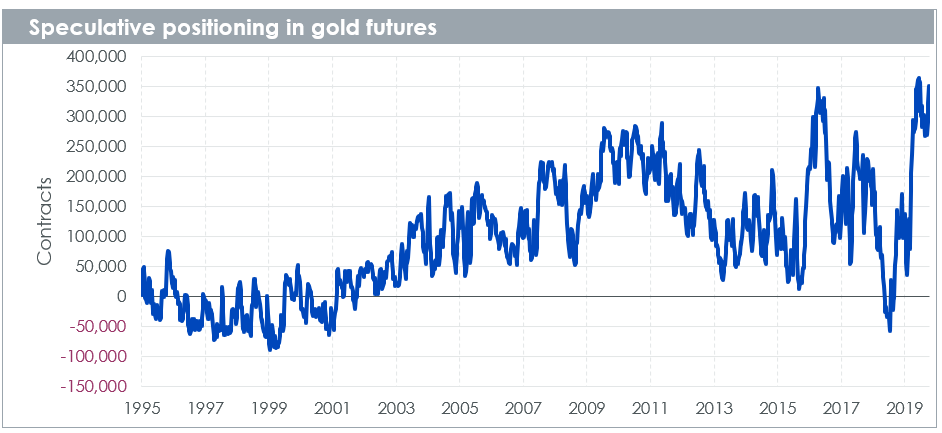

Why speculative positioning is currently elevated and will it last?

One of the key differences between our base, bear and bull cases is sentiment towards gold. Right now, positioning in gold futures is elevated after hitting an all-time high in September 2019. Why is sentiment towards gold so high and what could keep it there?

Source: Bloomberg, WisdomTree, data as of 31 December 2019.

Historical performance is not an indication of future performance and any investments may go down in value.

Positioning in gold futures has remained over 250k contracts net long for 28 weeks. That is the longest stretch of time (previously in 2016 it had been over that level for 21 weeks). The most recent reading of 351,088 contracts net long (31st December 2019) is the 4th highest on record, with the other three reading that were higher having taken place in August and September 2019 – at the peak of trade tensions between US and China. Markets are clearly anxious about the tensions in the Middle East today. The combination of trade anxiety and fear of military confrontation in Iran has drawn investors towards gold. Even though cyclical assets like equities are doing well, investors are building in hedges via gold. Military confrontation is the reason for the most recent spike in positioning, but even if this subsides, trade anxiety is unlikely evaporate easily this year. The sheer unpredictability of policy makers choices and the dire implications of political gambles going wrong are weighing on investors sentiment. It’s not that investors are expecting things to go wrong as a base case, but the risk is high and consequences are bleak, so it makes sense to build in hedges. Putting some more colour on this – what happens if trade wars spiral out of control and policy makers have to react? We know that traditional monetary policy has been taken to it limits and so more unconventional monetary policy may have to be deployed. What shape and form could that unconventional policy take? Could it increase apparent imbalances already in the economy or solve them? Could much needed structural reforms in aging and decelerating economies be put on the back-burner again as shovel-ready projects take up all the policy space and budgets? The European Central Bank and the European Commission are both currently under new leaders. With this could come a period of creative thinking in Europe’s policy institutions. The European Central Bank (ECB) is undertaking a strategic review and some speculate that more creative tools could be adopted at the end of the process. It could turn out that new tools are not even needed if the economy takes an upward turn, but just as in the Great Financial Crisis of 2008, new tools could be treated with suspicion. Gold is often the first post of call in times of market uncertainty.

Unfortunately, the answer to the question how long speculative positioning will remain elevated is therefore linked to how long trade uncertainty, military conflict concerns (and other geopolitical risks) will remain. For that we don’t have a clear answer, but our scenarios hopefully provide colour on what could happen to gold if positioning were to fall or remain elevated.

Related blogs

+ Gold: how we value the precious metal

+ Gold could rise to over US$1800/oz if geopolitical risks remain elevated

+ Gold above US$1400, where next?