Gilts, Bunds, Treasuries: how to hedge the downside

Trump’s US election win. Brexit. The inability of the ECB to contain the spike in German Bunds and Italian BTPs. All these recent events underpin the fresh bearish sentiment in fixed income. As an investor, it may be the right time to assess the downside risks of high-grade debt and to consider protection. But how? Using leveraged inverse (short) ETPs to position bearishly (“short”) to the bullish (“long”) position, can be one such way to access a simple, but effective strategy for hedging. In this piece, we explain how short Exchange Traded Products (“ETPs”) can be used to hedge exposure to UK government bonds (aka “Gilts”) and other high-grade government bond benchmarks including US Treasuries and German Bunds. Key to understanding how short ETPs perform as both hedging instruments and as a means to position bearishly is volatility, its impact on daily compounded returns and how rebalancing can work to protect capital in times of uncertainty. Short ETPs – how do they work? Investors can hedge their long Gilts exposure through the use of short ETPs. Short ETPs provide an inverse exposure to the underlying index. They rebalance on a daily basis and can be unleveraged or leveraged. For example, if 10Y UK Gilts fall by 0.20% in one day, an unleveraged short ETP tracking 10Y UK Gilts would rise 0.20% in one day. If the short ETP is leveraged, the daily return would be the inverse return of the underlying multiplied by the leverage factor. If in the same example the short ETP has a leverage factor of -3, then the return of such a 3x short ETP would be 0.6% (-3 x -0.2%). Against the background of this recent bearish sentiment in fixed income, Chart 1 shows how our range of Boost 3x short ETPs – which track the 10Y benchmarks of US Treasuries, German Bunds, UK Gilts and Italian BTPs – have performed recently.

Past performance is not a reliable indicator of future performance

In practice: Hedging Brexit uncertainty using Short ETPs tracking UK Gilts

The EU referendum earlier this year casted uncertainty – and continues to – over the UK economic outlook. Specifically, rising inflation expectations, a deteriorating trade and budget deficit, and the perceived risk to the “safe haven” status of Gilts, have all caused concern for investors.

Assuming a GBP100 investment was made in 10Y UK Gilts, we highlight two simple hedging strategies using 3x short ETPs with the goal to protect your investment.

1) Hedged, no rebalancing (buy and hold): one purchase of a 3x short ETP, the notional value of which equals the starting value of the long position (dotted orange line in Chart 2)

2) Hedged, with rebalancing: purchases and sales of 3x short ETPs, to adjust the change in its notional value to the change in the (market) value of the long position (straight orange line in Chart 2)

If you stay unhedged…

In the run-up to the EU referendum to date UK government bonds have been subjected to a marked reversal in investor sentiment. With the British vote to leave the EU seen as a risk-off trade by the market, 10Y UK Gilts (using rolling futures as a close proxy) prices rose to 8% from June to the end of August as yields fell approximately 60 bps to record lows of approximately 0.5% (see shaded area in Chart 2).

However, sentiment reversed decisively in September amidst a tough stance taken by the government to proceed with invoking Article 50. The bout of losses inflicted on Sterling given the potential pressures to the current account, the budget and inflation, have had a knock-on effect on Gilts. From their lows in August, yields on 10Y Gilts have risen by more than 70 bps to around 1.2% by the end of October which meant investors have lost about 4.5% over the period.

In the space of few months the losses incurred are equal to the what UK 10Y Gilts have delivered in average annual returns to investors since 2010. There remains lingering uncertainties over the kind of Brexit – whether it’s hard of soft – along with speculation of when Article 50 is to be invoked following the recent High Court ruling requiring the backing of Parliament to do so. It adds fuel to the notion that bearish sentiment in gilts is likely to persist.

Hedging strategy 1: Hedged - no rebalancing, buy and hold the 3x short ETP

A GBP25 allocation out of the long position and into the 3x short ETP would enable the investor to be fully hedged for one day, as the notional value of the short exposure is now GBP75 (3 x GBP25), which equals the value of the long position (i.e. GBP75). If the leverage factor was less (more) than 3x, then more (less) than a GBP25 investment in the 3x short ETP is needed to initially create a fully hedged position in 10 UK Gilts.

A price change, for instance of -2%, would protect the value of the investment over a one-day period, as the loss of value in the long position, GBP3 (GBP 75 x -4%), is offset by the gain in value of the short position, GBP3 (25 x -4% x -3).

How did the hedged position fare during the entire June to November holding period?

As shown by the dotted orange line in Chart 2, the value of the hedged position has remained relatively stable, with a total return for the period to be -0.36%, indicative of a limited impact the daily compounding had on the cumulative performance of 3x short ETPs and the hedged position. Over this period therefore, the buy and hold strategy did protect investors effectively.

However, what is evident from Chart 2 is that a buy and hold strategy will, due to reasons of compounding discussed earlier, cause the portfolio’s hedged position to drift away from the desired target. For instance, in the relative choppy uptrend, the value of the long position rose by more than what the 3x short ETP lost in notional value, causing the portfolio to become progressively under-hedged. In the choppy downtrend, losses in the long position exceeded the gains in the 3x short ETP, making the portfolio progressively over-hedged.

This is when rebalancing comes into play, as seen in the second hedging strategy below.

Past performance is not a reliable indicator of future performance

Hedging strategy 2: Hedged, with rebalancing, buy or sell 3x short ETPs to adjust the hedged position

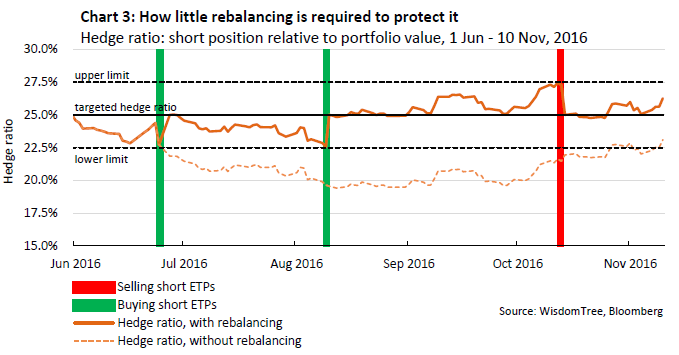

Limiting the portfolio from becoming over- or under-hedged can be achieved through rebalancing the hedged position. Shown by the straight orange line in chart 3, doing so would have resulted in a more stable hedged position than in the buy-and-hold strategy.

How much and when rebalancing is needed depends on the investor’s tolerance of how far the hedged position can drift away from the target before a rebalance is triggered. In a simplified example, we allow the targeted hedge ratio of 25% (GBP25 of the GBP100 initial investment allocated in 3x short ETPs), set at when the hedge is put on initially on 1 June, to fluctuate between the realised hedge ratios of 27.5% (the upper limit for being over-hedged) and 22.5% (the lower limit for being under-hedged). Hitting the upper limit or lower limits would trigger the rebalance.

When, in what direction, and how frequent rebalancing was triggered to achieve the stability in the hedged position, is shown by the vertical green and red bars in Chart 3.

1st rebalancing on 24 June 2016: the day when the results of the EU referendum came in favour of the UK leaving the EU: the sharp sell-off in equities drove investors to seek refuge in safe havens, causing prices of 10Y UK Gilts to spike and a move large enough for the hedged position to breach the lower bound of the target hedge ratio and trigger a rebalancing. The investor buys additional 3x short ETPs (see green bar on the left in Chart 3).

2nd rebalancing on 9 August: the day when the Bank of England bought a large amount of UK government debt in an effort to compensate for its failed attempt in receiving enough bids for purchases of high rated corporate debt as part of its corporate QE programme which was announced days earlier. 10Y UK Gilts rose on the action and similar to the 1st rebalance, additional purchases of 3x short ETPs worked to restore the hedge ratio (see green bar in the middle on Chart 3 middle).

3nd rebalancing on 13 October: the day when the upper bound of the targeted hedge ratio was hit following sharp falls in Gilts prices in previous weeks on growing fears of a hard Brexit, compounded by Sterling slump that has raising inflation expectations. Sales of 3x short ETPs worked to restore the hedge ratio (see red bar on the right in Chart 3).

Past performance is not a reliable indicator of future performance

Without rebalancing, the hedge ratio progressively dropped on rising Gilt prices (orange dotted line), making the portfolio increasingly under-hedged and positioning the investor as net long 10Y UK gilts. While favourable on rising markets initially, when the Gilts subsequently fell, the portfolio was under-hedged and did not sufficiently reap the gains it began accumulating in the 3x short ETPs to cover the growing losses in the long position.

With rebalancing however, the hedge ratio hovers within the upper and lower limits (straight orange line), with the actual hedge ratio reversing to the targeted 25% every time the upper or lower limit is hit.

Conclusion

There is no right or wrong way to constructing hedged positions and the examples highlighted above serve as simplified examples of how leveraged short ETPs could potentially be used as hedging instruments. Investors must understand that overall, the drivers of volatility of leveraged short ETPs depend on the type of market conditions/cycles they find themselves in, the kind of asset class leveraged short ETPs track and the leverage factor involved. Together they determine the effect of daily compounded returns to the cumulative performance of leveraged short ETPs held over periods longer than one day. Once fully understood, investors may consider using leveraged short ETPs as a means to construct hedges around asset classes. Investors sharing this sentiment may consider the following ETPs to hedge their exposures to fixed income.

+ Boost Gilts 10Y 3x Short Daily ETP (3GIS)

+ Boost Bund 10Y 3x Short Daily ETP (3BUS)

+ Boost Bund 10Y 5x Short Daily ETP (5BUS)

+ Boost US Treasury 10Y 3x Short Daily ETP (3TYS)

+ Boost US Treasury 10Y 5x Short Daily ETP (5TYS)

+ Boost BTP 10Y 3x Short Daily ETP (3BTS)

+ Boost BTP 10Y 5x Short Daily ETP (5BTS)