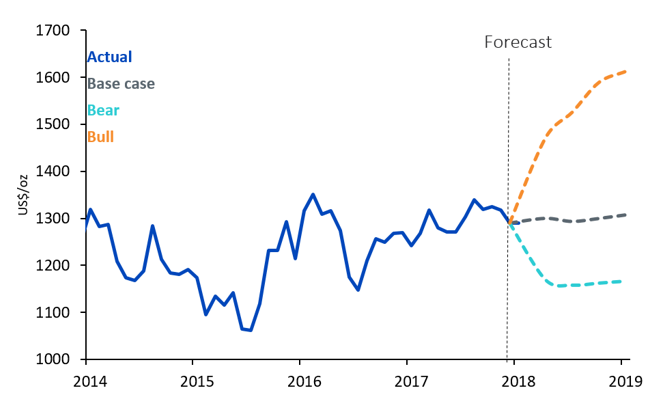

Gold outlook: geopolitical risk holding up prices for now

Gold wears many hats. At times it can be a monetary asset – an alternative currency to the US Dollar or Euro – whose value historically declines in periods of monetary tightening. Other times it can be seen as a safe-haven asset – the port of call for investors seeking refuge from the volatility that uncertainty breeds. Today gold seems to be wearing that second hat.

In fact for most of this year gold has been sporting its safe-haven hat. US government shutdowns, sabre-rattling between US/Japan and North Korea, the ratcheting up of a trade war between the world’s largest economies, interactions between Russia and NATO sponsors deteriorating back to cold-war tendencies, the potential return of sanctions against Iran and the proxy war between Saudi Arabia and Iran are few of the sources of investor anxiety. That’s all in the backdrop of cyclical assets experiencing periodic downward lurches after several years of serenity. In recent days the threat of military strikes in Syria have added to that anxiety.

In the absence of this second hat, we believe that gold would be trading much lower than the level US$1345/oz it was trading as of 16/04/2018. The interest rates in the US are rising. The latest Federal Open Market Committee (FOMC) minutes highlight that all participants agree that the US economy has strengthened, and that inflation is rising. Ex-chair Yellen - although no longer voting – remains influential and her belief is that the slack in the labour market has eroded. Although the FOMC seems willing to tolerate above-target inflation rather than undershoot, none of the participants believe the downside risks to price outweigh the upside (the first time that has happened since the Federal Reserve has published such data in 2011). The dispersion of dots in the ‘dot plot’ (the map of the FOMC participant’s views on where policy rates will end the year), has shifted significantly from December 2017, with an equal number of participants now expecting three more rate hikes as those expecting two (in addition to the rate hike in March). It will likely only take a small nudge to get more Fed participants to expect higher rates.

Inflation to gain momentum

We expect US inflation to rise to 2.6% by December 2018 (from 2.4% in March 2018). Higher inflation generally supports gold prices. These forecasted levels of inflation will likely be uncomfortably high for the Fed, but given the lags in policy and price response, there is little the Fed can do next year to stop it (the inflationary pressure has been built up in 2017). However, we believe at least two more rate hikes in 2018 will be required to keep inflation expectations sufficiently anchored and a third rate hike should not be ruled out given the shift in Fed thinking mentioned above. The higher interest rate environment should be gold price negative.

Source: Bloomberg, ETF Securities, data available as of close 12 April 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

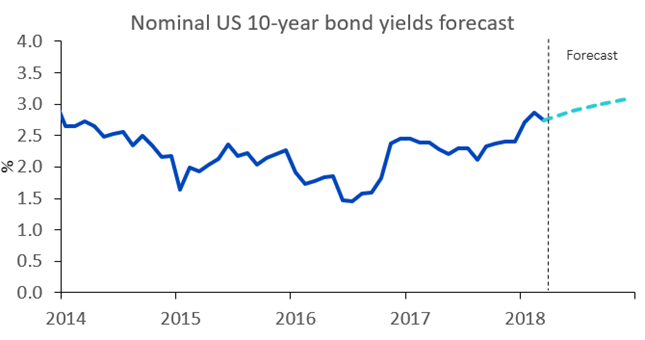

US Treasury yields

During the rate tightening that took place in 2017, the US Treasury yield curve has flattened. While there have been 75bps of policy rate increases since December 2016 and December 2017, nominal 10-year Treasury yields had fallen from 2.60% to 2.34%. Treasury yields have started to steepen this year, with the 10-year yield at 2.79% currently. We expect 10-year Treasury yields to rise to 3.1% by the end of 2018.

Source: Bloomberg, ETF Securities, data available as of close 12 April 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

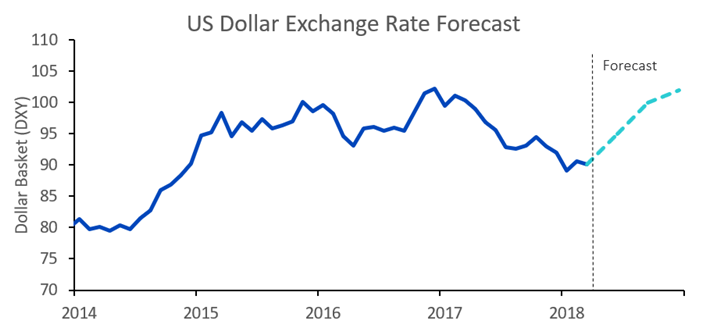

US Dollar

We expect the US Dollar to appreciate, reversing the weakness that we have seen in 2017. We expect the DXY (the trade weighted US dollar index) to appreciate to 101 to 103 by the end of 2018 from 90 currently. A lack of progress in implementing pro-growth policies that the Trump Administration had promised, a lack of tax and budget reform and a generally stronger Euro and Yen had weighed on the US Dollar in 2017. Some of these trends will continue to drag on dollar performance in 2018, but rising interest rates will lend some support. We believe that the policy divergence between the Federal Reserve, European Central Bank and Bank of Japan will become more pronounced as the market becomes increasingly disappointed by the pace of tapering by the latter two central banks. That is likely to reverse some of the strength in the Euro and Yen.

Source: Bloomberg, ETF Securities, data available as of close 12 April 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Geopolitics appears to be the main swing factor

Given our view of the Fed raising rates 2-3 more times this year, US Dollar appreciating, and Treasury yields rising, we expect gold prices to decline in the absence of geopolitical risks remaining elevated. Slightly higher inflation alone won’t prop up gold prices unless the Fed is looking like it has lost control (which we don’t believe). In our modelling framework, market fears around geopolitical risk is gauged by speculative positioning in the gold futures market. In our base case model scenario, where geopolitical risks subside, speculative positioning could normalise from above 200,000 contracts net long two weeks ago to around 120,000 contracts. In that scenario gold prices are likely to decline to US$1275 to US$1285/oz. However, leaving all other assumptions the same, gold prices could rise to US$1370 to US$1380/oz if speculative positioning were to rise to 250,000 contracts net long.