Utilising ETF Implied Liquidity to properly position ETFs in portfolios

Liquidity is one of the most misunderstood terms in the ETF world. So what is it anyway? In general, it’s defined as the ability to quickly convert an investment into cash with as little friction or transaction cost as possible. Intra-day liquidity is one of the most important factors separating mutual funds from ETFs. And because ETFs, like stocks, are traded on exchange investors often equate volume with liquidity. This would be a mistake. The liquidity of an ETF is not defined by the volume it trades on a given day and is not indicative of the potential future liquidity of an ETF. ETF volume is a historical number. In addition, assets under management are not indicative of the potential liquidity of an ETF. To put it simply, ETF Liquidity is a function of the accessibility of the assets in the underlying basket with an additional layer of liquidity provided by daily trading volume of the ETF on exchange.

ETFs are open-ended vehicles, which means that new shares can be created and redeemed on demand. Because ETFs are listed on major stock exchanges (the secondary market), but also have a robust primary market process for creation and redemption, investors can trade these ETFs intra-day, very efficiently, regardless of the daily volume of the ETF. New shares will be created on the primary market to fulfill demand on the secondary market. First and foremost, an ETF is a wrapper that holds a basket of underlying securities or provides exposure to an underlying benchmark. The liquidity of an ETF is derived primarily from this underlying basket of securities.

Investors should not rule out innovative and valuable strategies based on ETF volume or AUM. These are some of the traps investors may fall into:

- Thinking all ETFs behave similarly and are best utilised in the same way

This is important because strategic investment products tend to have lower daily volumes over tactical ones. Investors utilising strategic ETFs are typically making longer term investments. These ETFs typically don’t track the main benchmarks, but rather proprietary indices positioned to help investors achieve better risk-adjusted returns over time. These products are more likely to have lower daily ETF volumes as investors are not buying and selling very often in these products. Again, this doesn’t not mean the product is illiquid, but rather that it trades infrequently on exchange. The liquidity will come from the underlying basket and is aided by the structural efficiencies of the ETF wrapper. These strategies should not be omitted from an investment universe based on volume metrics.

- Using the US markets as a benchmark for comparison for Europe

The reality is that the European ETF market is very different. It is a lot more fragmented than the US one: there are a number of issuers across many countries launching and listing products on different exchanges and in different currencies. That same ETF can then be cross listed four times and listed in four currencies. ETF volumes don’t consolidate on one exchange or one ticker, unlike the US where ETFs are listed and settled in USD and a consolidated volume number is published.

It’s also well known that off-exchange or over-the-counter (OTC) trading is much higher in Europe than in the US. This is unfortunate from a customer perspective, because they obscure the view of what is actually going on in the markets. In 2016 YTD, approximately 74.5% of all ETF trading on the London Stock Exchange occurred OTC[1]. These volumes don’t necessarily hit the exchange in the printed volume figures which leads to a distorted market view. In this case, ETF volumes aren’t actually low, they just look like they are.

So how can an investor actually quantify the underlying liquidity of an ETF?

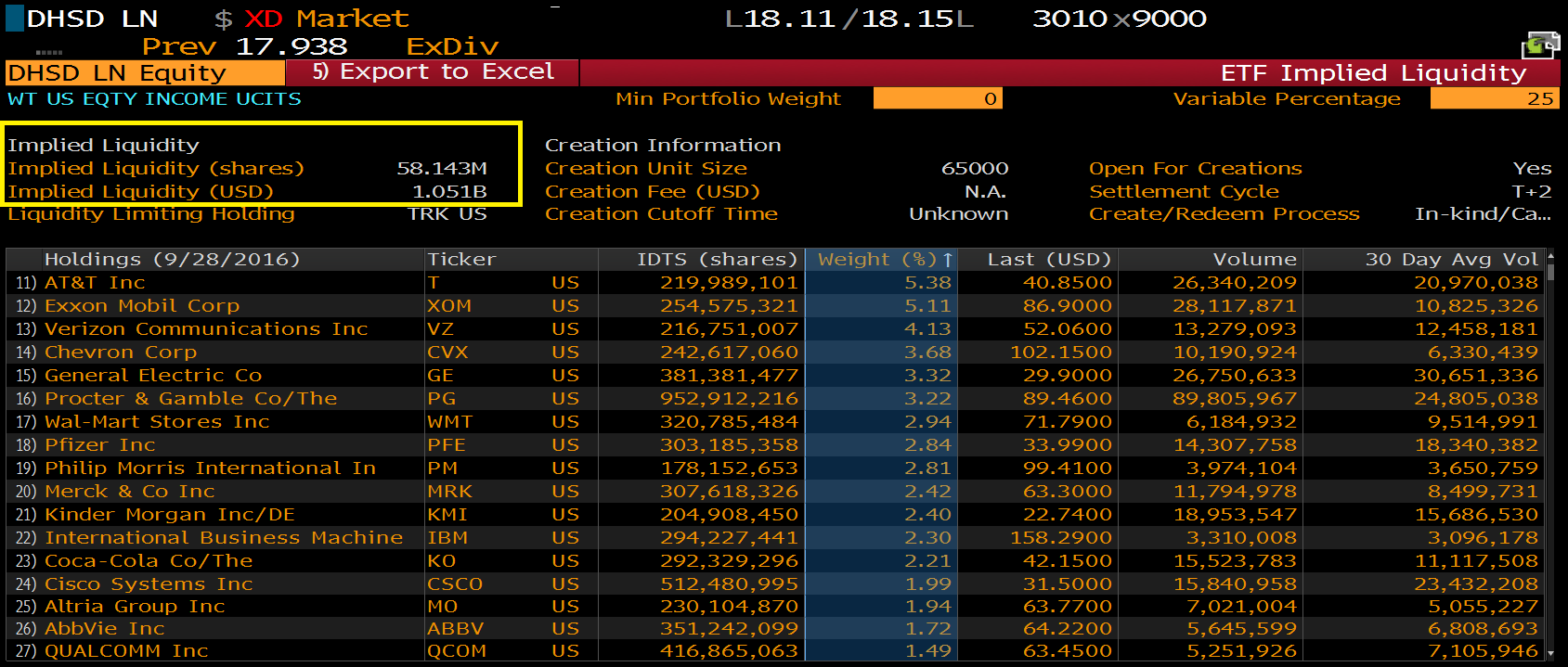

The ETF Implied Liquidity metric is the only way for investors to gain an understanding of the potential liquidity of an ETF. Implied Liquidity is “a representation of how many shares can potentially be traded daily in an ETF as portrayed by the creation unit.” This number is helping investors understand in a tangible way, how many shares (or USD, EUR, GBP or CHF) of an ETF they can trade on a daily basis without having a price impact on the underlying securities.

In the example below, you can see the WisdomTree US Equity Income UCITS ETF (DHSD LN) Implied Liquidity is over $1bn USD (over 58m shares). This indicates to an investor that without having a price impact on any of the underlying securities, you can still easily trade over $1bn USD of DHSD LN on a daily basis when looking at the liquidity of the underlying securities and extrapolating that into ETF terms. This presents very different understanding of potential use of the ETF than is presented from the actual trading volume of the ETF on exchange.

Source: Bloomberg

In addition to understanding Implied Liquidity, you should also ask some questions of the ETF issuer’s Capital Markets team in order to understand the potential investment size that can be made in an ETF:

- How liquid and accessible are the actual underlying securities?

- How easy is the underlying basket to hedge?

- Are there correlated hedges? Are there correlated derivatives or products that can be used to provide liquidity in the ETF?

- Are there taxes or ticket charges applied in trading the underlying securities?

As the ETF industry continues to grow, there will be new innovative products brought to market. Most will not enter the market on Day 1 with large AUM or volume but savvy investors should look for those products that provide opportunities for their portfolios – those ETFs which resonate with strategy, which fill an investment need – rather than looking solely at trading volume. Ultimately, ETFs as a structure are robust, transparent with the advantage of being able to move in and out of positions quickly and efficiently when need be – thanks to the efficient features of the structure and of the ETF trading process.

[1] London Stock Exchange: ETF&ETP Monthly Trading Data by Security, http://www.lseg.com/areas-expertise/our-markets/london-stock-exchange/fixed-income-markets/listed-products/etfs