The challenge ahead for Europe’s oil and gas sector

In Certain sectors have a higher sensitivity to Europe’s recovery, we discussed two struggling sectors that may see their fortunes revived as Europe’s economy heals from the pandemic. We now turn to a sector that’s currently booming but faces a choppy road ahead. Tactical investors, who are prepared to take both long and short positions, are often on the lookout for such inflection points.

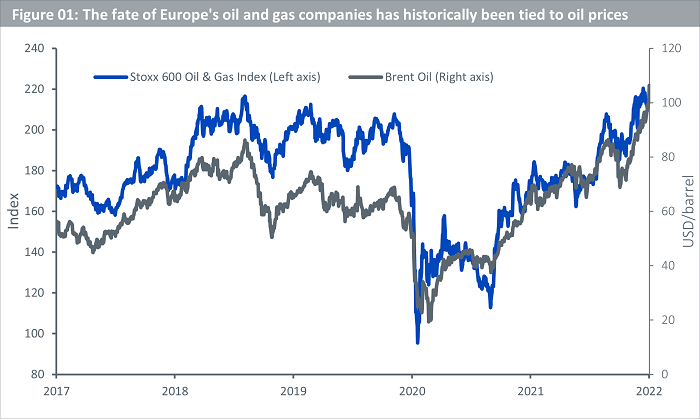

To most observers, even those with a keen interest in financial markets, the historic chart of the oil and gas sector would be indistinguishable from oil prices – if the two weren’t correctly labelled. Figure 01 below illustrates this. This is understandable given profit margins for oil and gas producers rise when consumers can be charged higher prices for the same product.

Source: WisdomTree, Bloomberg, as of 02 March 2022.

Historical performance is not an indication of future performance and any investments may go down in value.

Taking a view on oil markets, therefore, is synonymous with taking a view on the sector.

What can we expect from oil prices?

As of this writing on 03 March 2022, Russia’s invasion of Ukraine is in full swing with the crisis putting oil prices on boil. In February, before the conflict began, markets began pricing in a geopolitical risk premium. In March, with the conflict intensifying, markets are beginning to price in an outage of supply from Russia – the second largest oil exporter in the world.

This has created a binary set of scenarios for oil prices in the near term. If the conflict continues to escalate, oil prices will inevitably rise further. If, however, peace is restored, some of the risk premium baked into prices will also erode.

With that, let us assume that tensions subside and focus returns to fundamentals. What happens then? In such a scenario, the relative trajectory of demand and supply growth will be noteworthy. According to the International Energy Agency, world oil demand is set to rise by 3.2 million barrels per day (mb/d) in 20221. Despite this, IEA believes that oil markets will go into a surplus later this year. This is because OPEC+2 has enough spare capacity to increase its supply by 4.3mb/d while non-OPEC+ producers (like the United States and Canada) could add 2mb/d of supply.

Source: WisdomTree, US Energy Information Administration, Refinitiv. Last updated on 08 February 2022.

Historical performance is not an indication of future performance and any investments may go down in value. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

This spare capacity is the key differentiator compared to 2008 when oil prices breached $100/barrel (see figure 02 above). Furthermore, if sanctions on Iran are lifted, another 1.3mb/d could be added on relatively short notice quenching any additional demand3.

Having said that, OPEC in its recently concluded meeting on 02 March has decided not to increase the pace of supply additions beyond the current schedule of adding 400,000 b/d each month this year. In the wake of the ongoing war, this could exacerbate the tightness in oil markets in the near-term.

Oil prices may, therefore, heat up further before cooling down.

The energy transition

In the long run, reliance on fossil fuels is inevitably going to decline as the world transitions towards renewables. If the pledges from world leaders at last year’s United Nations Climate Change Conference (COP26) weren’t enough, the Russia’s invasion may have further catalysed the transition. Europe’s dependence on Russia for energy may be seen a vulnerability that needs to be addressed. Russia accounts for around 27% of Europe’s crude oil and 41% of natural gas imports4.

Since the escalation of tensions, Germany has put a pause on Nord Stream 2 – the pipeline from Russia to Germany under the Baltic Sea which was meant to double the capacity of Russian gas exports to Europe. Now, in the very first instance, this raises the prospect of further tightness in Europe’s gas supply. But Germany has also announced its intention to turbocharge its push for renewables with plans to source almost all its power from green sources by 2035. Other governments may follow suit. Regardless of ties with Russia, it’s the right thing to do in the face of climate change.

Where does that leave the oil and gas sector? Parts of the sector may be able to reinvent themselves as renewable energy companies. Companies like Shell and BP have got net zero pledges in place and more focus on renewables is on the agenda. But such a complete transformation of business models will neither be overnight, nor be possible for all companies within the sector. And in the meanwhile, scrutiny from investors on oil and gas companies is also expected to rise given ESG5 considerations.

Expect volatility

Oil bulls don’t just cite geopolitics to support their views. They also highlight that capital expenditure in upstream oil and gas (the part of the supply chain closest to extracting the natural resources) has been on the decline faster than the shift towards renewables. Indeed, global oil and gas upstream capital spending fell from just under USD 800bn in 2014 to around USD 500bn in 2019. This downward trend is only expected to accelerate given investing in oil and gas has gone out of vogue. But the world still needs energy. And until renewables can fulfil the entirety of demand, oil and gas will still be needed.

What this means is that the energy transition is unlikely to be linear across all fronts. The trajectory of the oil and gas sector is also unlikely to be a straight line in either direction. Even beyond the geopolitics currently in play.

So, we may continue to see volatility in the oil and gas sector going forward. This takes us back to where we started – volatility creates more inflection points – a feature tactical investors are always looking out for.

Investors have options

When it comes to expressing directional views on oil and gas, investors have choices. One option is to gain an exposure directly to commodities. Most investment products typically achieve this through futures. Alternatively, investors can access the space through the oil and gas sector – given its strong correlation with energy prices.

Sources

1International Energy Agency Oil Market Report February 2022.

2The Organization of the Petroleum Exporting Countries and its partners

3International Energy Agency Oil Market Report February 2022.

4European Commission estimates based on 2019.

5ESG stands for Environmental, Social, and Governance

Related blogs

+ Certain sectors have a higher sensitivity to Europe’s recovery